Buying your first home

We're here to help make things as simple and seamless as possible.

Our home loans

- Discounted home loan rate

- Offset sub-account available for +0.10%^

- 10% deposit minimum

- Discounted green home loan rate

- Offset sub-account available for +0.10%^

- 10% deposit minimum

- Discounted solar home loan rate

- Offset sub-account available for +0.10%^

- 10% deposit minimum

- $5,000 interest free Visa debit card

- Unlimited free redraw

- 20% deposit minimum

Get ready to enter the property market.

The first thing you’ll need to do is decide what you want to buy, so consider the location, whether you’d prefer a house or unit, a new home or existing home, and whether you’ll live in it or rent it out.

Next, get an idea of how much you can afford. Will you be buying by yourself, or with someone else? How much have you saved for a deposit? What are your income and expenses looking like?

It’s also important to research all the costs which may be involved with buying your first home, like stamp duty, Lenders Mortgage Insurance, Property valuation and conveyancing.

When you’ve done your research, it’s time to get pre-qualified. With loans.com.au, you can apply online in just minutes. This will give you a guide of how much you can borrow. From here, we can help you apply, upload your documents, complete the valuation of your property, and get your loan approved so we can return your documents and you’ll settle.

No matter what stage of the process you’re at, we’re here to help.

Why do people choose us for their first home?

Low interest rates

Being an online lender with fewer overheads means we’re able to pass on the savings to our customers.

Australian based

Get help when you need it from our friendly team of Australian based, lending specialists.

Flexible options

Looking to save with an offset, or make extra repayments with a redraw? We have a full range of loan features to suit your situation.

Award winning

We keep on winning awards for our products, innovations and customer service, year after year!

Our home loan application process

Application

Simply fill out your home loan application online by entering some of your details, or chat to one of our friendly lending specialists over the phone and they can complete your application for you.

onTrack

After your application is complete, use our system we call onTrack on your desktop or device to add your documentation such as payslips and bank statements, and track the progress of your application.

Speak to specialist

You will then have an appointment with one of our lending specialists to organise your preliminary approval of your loan, and help you progress through the home loan approval process through to settlement as quickly as possible.

Signing document

Check onTrack to received your final approval, mortgage documents and loan agreement. You must sign these and return them in to onTrack.

Settlement

Your loan will settle and you’ll start saving with your new loan rate, and get your keys to your new dream home!

Access your account

Once settlement is complete, we will send your login credentials to start managing your payments in the Smart Money app.

Common home loan questions

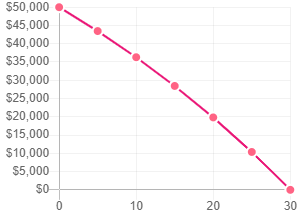

Home loan repayment calculator

Use our home loan calculator to estimate what your monthly mortgage repayments could be. Whether you're refinancing or just wanting to understand how much you can afford, all you have to do is enter how the amount you would like to borrow, interest rate, home loan term, payment frequency, and repayment type (either principal & interest or interest-only).

Your estimated repayments are

Get a loans.com.au super low rate you’ll be celebrating for years!

Get started

Ready to enter the property market and buy your first home? Simply apply online or chat to a lending specialist and they can do the hard work for you. We make the process easy so you can get the keys to your first home as soon as possible.

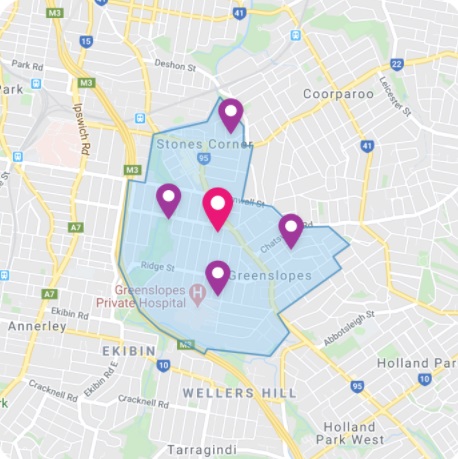

Get free property & suburb insights

To help you find the perfect home, we'd like to give you a free loans.com.au Comparative Market Analysis (CMA) property report, a breakdown of information about the property you are considering, including previous sale prices.

Estimated property value

An indication of how much the property is worth, based on factors including recent sale prices for comparable properties in the area.

Property mapping

An aerial photo of the property and its immediate surrounds, plus maps of the street & the property in relation to points of interest and facilities.

Properties sold in the area

You will be able to see details of recently-sold properties in the area including the date they were sold, land size, number of bedrooms, number of bathrooms and garage size.

Market comparison

Detailed information about nearby properties currently listed for sale or recently sold, including their first and last advertised price and days on the market.

Median sale prices in the area

The median sale price for homes in the area and how it has changed each month in recent years.

Suburb insight

Information about the suburb's demographics, such as household occupancy, household income and household structure.

Useful Resources

Guide on buying your first home

Most people have questions as they start on the home buying journey, so we have pulled together some articles to help you. From information on our easy steps to apply for a home loan, to advice on pre-approvals and buying a home, you can find it here..

What is the average house price in Australia?

The steadily growing house prices can be attributed to several factors including inflation, population growth, supply and demand, interest rates, and tax policies, to name a few.

Stamp duty explained: state-by-state guide

Stamp duty is a tax imposed by state governments in Australia on the purchase of assets such as real estate. This includes title transfers in real estate, vehicles, insurance policies and home loans.

Pros and cons of buying off-the-plan

Wondering if you should buy off the plan? Here are some pros and cons of buying a property off-the-plan.

Tips for buying a house alone

Guide to Buying Your First Home

Difference between official cash rate and mortgage interest rate

Expression of Interest: What does it mean?

5 tips to buy a home on a single income

Buyers Guide to Finding the Perfect House

Buying at auction vs private treaty

Moving house checklist

First Home Buying Incentives