Is an offset sub-account worth it?

An offset sub-account is a great feature for borrowers and can help you save time and money off your mortgage.

An offset sub-account is a great feature for borrowers and can help you save time and money off your mortgage.

To work out if an offset home loan is right for you, you first need to understand what it is.

What is an offset sub-account?

Our offset sub-account is linked to your home loan (whether that's a split home loan with offset, or interest only loan with offset) where you can put money such as your salary and savings into.

That money is then 'offset' against the balance of your home loan, so you only pay interest on the difference between the loan amount and the amount in your offset sub-account. This means you pay off the loan faster and with less interest.

Putting money into our offset sub-account is like making extra mortgage repayments - except you can conveniently redraw the money using a Visa Debit card as if it were a daily transaction account.

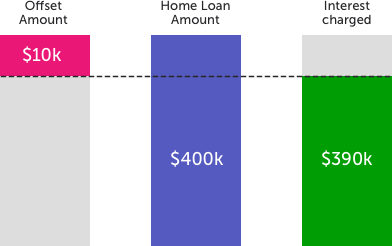

Here's an example: Let's say your loan balance (the amount you owe us) was $400,000 and you had $10,000 in your offset sub-account . Instead of calculating the interest on a home loan balance of $400,000, we would only calculate it on a balance of $390,000 ($400,000 - $10,000).

Your monthly repayment stays the same, but you're repaying the loan faster and paying substantially less interest.

In this hypothetical situation, interest is applied to $390,000 instead of the full $400,000 owed. The offset money acts like extra mortgage repayments, shortening the life of your loan. And a shorter loan means less interest paid.

As the balance in the offset grows, the amount you save on interest grows too.

It's important to note that our offset sub-account is 100% offset. This means we take into account all of your money in your offset sub-account when we calculate your benefit. Not all lenders do this.

Offset calculator

Use our offset calculator to calculate the time and interest you can save on your mortgage when you put some money into our offset home loan.

Is an offset sub-account worth it?

An offset home loan can be a great way to save thousands of dollars of interest on your home loan. But it's still important to weigh up your individual circumstances to determine if an offset home loan is right for you.

Benefits of offset accounts

1. Pay less interest on your home loan

To accumulate significant savings, the amount of money held in the offset sub-account must be consistently at a reasonable level ($150 isn't going to cut it). To maximise the amount that is offset, many people deposit all their salary into it. They can then spend the money using a linked Visa Debit card, just as they would with a transaction account.

Some other people use a credit card for all their expenses throughout the month and then make a lump sum payment from the offset sub-account once a month at the time 'due' from their credit card provider to balance the credit card balance back to $0 (avoiding interest charges and fees from the credit card).

However, there is an interest rate premium involved with an offset home loan. This is why it's important to ensure this doesn't end up costing you more than the amount of money you save.

To avoid that problem, you need to maintain a reasonable ongoing balance in it - otherwise it may be more worthwhile to go for a streamlined variable loan and get a slightly lower interest rate.

You can still save on interest by making extra repayments into the loan, and you can withdraw the money at no cost if you need it in the future, though you won't have the convenience of a Visa Debit card.

For some, the benefits of a slightly lower home loan interest rate and lower loan term can outweigh the benefits of an offset. But for others who can maintain a strong balance in their offset sub-account, the benefits of saving thousands of dollars in interest is more valuable.

2. Maximise your savings

Offset accounts can be a much more beneficial place to store your savings than a standard savings account. Offset accounts don’t technically have an interest rate that earns interest. Instead, your offset sub-account offsets your home balance using your home’s existing interest rate, which is usually much higher than the average savings account.

While you might only earn a marginal amount of interest in a savings account, that money tends to work much harder in an offset account.

3. An offset sub-account is flexible, so you can keep extra funds at hand

A good offset account can make your home loan a much more flexible product: You can deposit your salary straight in there instead of a regular bank account, you can withdraw the payments as required, and allow you to pay your bills from it.

From fund emergency expenses to things like holidays or home renovations, how you use the money saved is up to you.

4. Offset accounts can provide tax benefits for investors

Interest earned, such as interest in a savings account, is usually taxed at your marginal tax rate as it is considered income. Offset accounts on the other hand don’t technically earn interest, and as such aren’t taxed as taxable income.

So in addition to not paying tax on the amount in the account, you can also save thousands of dollars off your loan.

At the end of the day, it's important to weigh up your individual circumstances and financial situation to determine whether an offset home loan is right for you.

Best ways to use an offset account

To make the most of your offset account, it's best to put any savings straight into your offset where it can work harder for you than it would in a savings account or term deposit.

You can also set up regular savings payments into your offset account if you have a savings goal like a holiday, and withdraw that money when you're ready to use it.

If you can get a debit card with your offset account and have online access to payments, it's a good idea to use your offset as your default transaction account and ask your employer to deposit your income directly into your offset account where possible to maximise your savings.

Interest is calculated daily on an offset account, so every dollar you can put into it will maximise the amount of interest saved on your home loan.

How much money do you need in an offset account to make it worthwhile?

Ideally, the more money you can put into your offset account and consistently keep it in there, the better. In most cases, it's recommended to have at least $10,000 in your offset account to break even after the extra expenses of an offset account which includes 'package fee' or 'offset account' fees.

Check out loans.com.au’s 100% offset sub-account with VISA debit access

The more money you have in an offset facility, the less you can pay overall and the more time you can save. If this sounds good to you, then why not take a look at loans.com.au’s 100% offset facility with VISA debit access. This offset facility is a flexible added feature to many of our home loans that allows you to offset 100% of your facility’s balance against your loan balance, with no monthly or ongoing costs and easy access to your money via online banking, ATMs and a special VISA debit card.

Apply now or book an appointment with one of our friendly lending specialists to learn more about this useful home loan feature.

FAQs

Does an offset sub-account reduce your monthly repayments?

Your monthly repayments will generally remain the same despite the fact you are paying less in interest. This is because more money in each repayment is going towards repaying the principal portion of your loan, meaning you could shave a significant amount of time off your loan term.

Is an offset sub-account better than a savings account?

Generally speaking, it's better to keep your savings in an offset account because your savings will work harder for you than if they were sitting in a regular savings account. Money in an offset account is 'offset' against the balance of your home loan, so you only pay interest on the difference between the loan amount and the amount in your offset sub-account.

This means you pay off the loan faster and with less interest. The ATO also doesn't charge tax on interest earned on the savings held in an offset account, whereas they do if it's held in a regular savings account.

How much can an offset facility help you save?

As mentioned earlier, an offset facility can help you save money on your home loan. How much? Well, it could be thousands depending on how you use it.

Let’s use that example from before: A $400,000 home loan with $50,000 in an offset facility. If:

-

The loan’s interest rate is 3.00% p.a (variable);

-

The loan term is 25 years;

-

The repayment frequency is monthly; and

-

You put the $50,000 into the facility after 2 years

Then you would reduce your loan term by around 4 years and save almost $44,000 in interest over the loan term.

This is much more than you'd earn in a savings account, although it’s impossible to say whether savings account rates will change over that same time period. You could also save much more over the life of your loan if you make consistent contributions to the offset facility.

Use our home loan offset calculator to work out how much you could save on your home loan.

Find out in under 2 minutes if you qualify for one of our home loans.

About the article

As Australia's leading online lender, loans.com.au has been helping people into their dream homes and cars for more than 10 years. Our content is written and reviewed by experienced financial experts. The information we provide is general in nature and does not take into account your personal objectives or needs. If you'd like to chat to one of our lending specialists about a home or car loan, contact us on Live Chat or by calling 13 10 90.