Even when you have done it before, buying a new home can be daunting. There are so many different challenges to overcome including finding a home, buying it, and getting the best value home loan. If you already own a home you may also have the added challenge of selling that home.

To help you succeed we have created this step by step guide to the process.

1. How much can you afford?

Before you start looking for a property you need to work out how much you can afford to pay so you don't waste time on houses in the wrong price range. This will be determined by a number of factors.

Value of your current home – If you already own a home, how much money would you be left with if you sold it and paid off the mortgage? That sum is your equity. Whether you plan to sell your current home or retain it as an investment, the amount of equity you have in it will be a big influence on how much you can borrow. If you sell before buying, you will know how much you have but if you plan to buy first and sell later, you and your new lender will have to make an estimate

Buying by yourself – if you are buying by yourself the amount you can borrow will be determined by your finances alone.

Buying with somebody else – if you are buying with somebody else, be it a spouse, partner or family member, the amount you can afford to borrow will be determined by both of your finances.

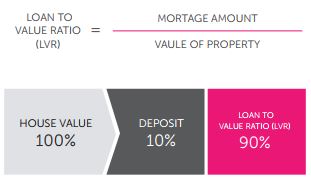

Your deposit – when you come to buy a home the size of your deposit is very important for several reasons:

-

100% loans are not available anymore. Most lenders will want you to put down at least 10% of the purchase price of the property. The rest – 90% of the purchase price of the property - can be financed using a home loan.

-

A larger deposit may mean a lower interest rate. The larger the deposit the lower the risk to lenders so they may charge you less.

-

Avoid Paying Lenders Mortgage Insurance - If you can put down a deposit of 20% or more, you can often avoid paying "Lender's Mortgage Insurance" (LMI). LMI protects the lender – not you, if you cannot repay your loan so avoid it if you can.

Income – The size of your income has a big influence on how much you can borrow because the more you earn the more you can afford to repay. Make sure you include and document all of your sources of income when you apply for a loan including salary, rent, interest, and business income.

Expenses – Your lender will also want to know your expenses because it helps them assess how much you have left over to make loan repayments.

2. Other costs to consider

Buying a house isn't just about paying the price of the property. The other costs also add up.

|

|

|

|

|

|

|

|

3. Selling your current home

If you plan to sell your current home you will need to consider the issues below.

Agent - Your real estate agent will be in charge of advertising, showing and completing the legal requirements of selling your property, so choose carefully. Make sure you interview multiple agents and seek word of mouth recommendations.

Private sale or auction - You and your agent will need to work out a plan for listing, showing and selling your property, including whether to sell privately or at auction.

Price - Your property's location, size, age and features will be factors in setting the price along with the current market and area trends.

Sell first or buy first – If you buy first you will own two homes at once, increasing the amount of debt you have to service. There is also the risk that your current home won't fetch as much as you expected, leaving you with more debt than you anticipated. On the upside, you can move straight into your new home. By contrast, if you sell the home you live in first you are less exposed but you have to finding somewhere to live until you can buy a new home and move in.

4. Getting pre-qualified

You can save yourself a lot of time and heartache if you pre-qualify for a loan before bidding on a home.

What is pre-qualification - Also known as conditional approval or preliminary approval, pre-qualification is an offer from us to lend you an agreed amount, subject to full approval. Pre-qualification remains valid for four months. To gain full approval you will need to supply more supporting documents and updated information.

Apply online - You can apply to pre-qualify with loans.com.au in just a few minutes by visiting our website.

Know what you can offer – Once you have pre-qualified you will know what you can offer a seller or what you can bid at auction. This means you can avoid wasting time looking at properties in the wrong price range and that you can bid with confidence.

5. Making an offer

There are two ways to buy a property in Australia. You can make an offer to purchase via a contract, or by bidding at an auction.

Private sale - Most residential properties in Australia are sold by making a private offer via a contract to purchase. Using this method, the owner sets the price they would like to get for their property. You put in an offer, which is usually below the asking price and negotiate as necessary with the seller from there by writing your offer on the contract and giving it to their agent. Offers pass back and forth until you and the buyer agree on price and terms and exchange contracts. You pay a deposit, typically 10 per cent of the selling price, and there is a coolingoff period. The cooling-off period allows you to complete final legal, building and financial checks but if you do back out of the sale you will most likely forfeit a small part of you deposit. When you buy via a contract offer you will typically also include clauses in the contract for finance and a building-and-pest inspection. These allow you to cancel the purchase without penalty if you cannot get acceptable finance or if the building and pest report has serious faults.

Auction – A property auction is a public sale usually conducted by an agent acting as an auctioneer. It is governed by strict rules. The auction is advertised for a specific place, time and date. Prospective buyers bid and the property is offered to the highest bidder. There is an advertising campaign with open house inspections for several weeks leading up to the auction date. When a property is sold at auction, the owner sets a reserve price – the minimum for which they will sell the property – and prospective buyers make their bids, with the property going to the highest bidder over the reserve price. The most important thing to remember is that there is no cooling-off period. You will also need to provide a substantial deposit on the day of the auction if you are the winning bidder. This is usually paid by cheque.

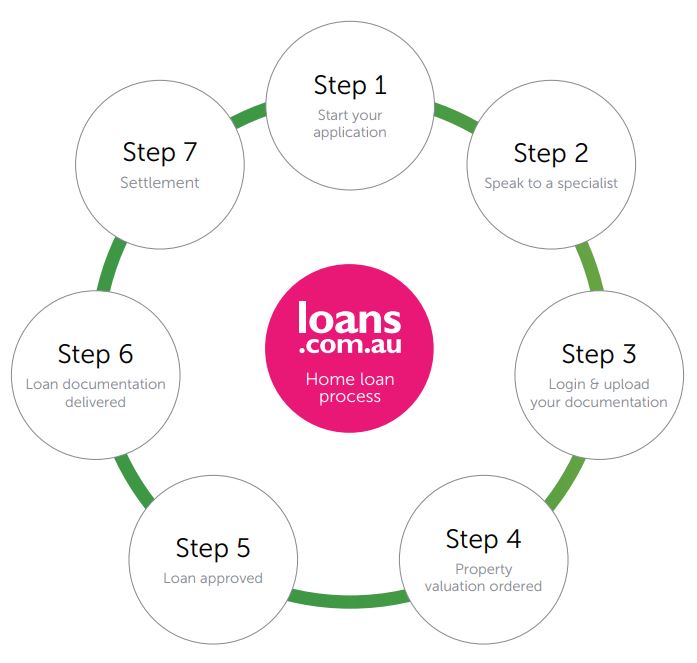

6. Our home loan process to settlement

Now you have made an offer and had it accepted either at auction or through a private sale, this is what happens at loans.com.au through to settlement.

Just follow the simple steps below to lock in a home loan with a super-low rate.

READ OUR HOME LOAN PROCESS

At loans.com.au we are proud to offer one of the most competitive interest rates in Australia for customers who want to buy a home.

You could save thousands of dollars on your home loan and pay it off sooner with loans.com.au.

Benefits include:

-

Award-winning home loans packed with features

-

A game-changing online model which means we can pass on ultralow interest rates to our customers

-

Simple online application process with our innovative OnTrack system

-

Borrow safe in the knowledge that we are secure, powered by Firstmac, which has been in business for over 38 years

Apply now To find out how much you can borrow, just use our handy borrowing power calculator.

If you are ready to apply for a loan, you can get started now by filling out one of our easy online applications here. It only takes a few minutes.